September started negatively for Wall Street as the main indexes declined over 1% on Tuesday. Investors were cautious, focusing on the latest economic data, remarkably subdued factory activity reports, and looking ahead to a series of labor market updates that could influence the Federal Reserve’s monetary policy decisions. The S&P 500, Dow Jones, and Nasdaq all saw significant drops, with the tech-heavy Nasdaq hitting a three-week low.

Factory Activity Remains Subdued

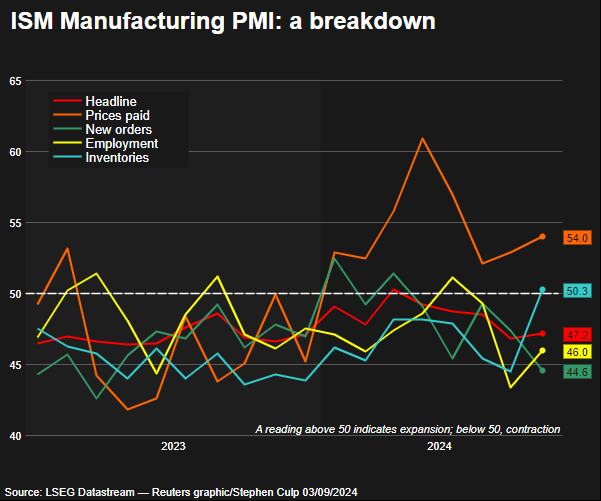

A key indicator of U.S. manufacturing showed a slight improvement in August after hitting an eight-month low in July. While there was some positive movement in employment within the sector, the overall trend continued to reflect sluggish factory activity. The S&P 500 industrials sector dropped more than 1.6% on Tuesday, with industry giants like Caterpillar and 3M contributing to the downward trend. As Josh Jamner, an investment strategy analyst at ClearBridge Investments, noted, “The softer PMI surveys that were released this morning accelerated a little bit of profit-taking that had played out.” This sentiment reflects the concern that the current data does not align with hopes for a soft economic landing.

Tech Sector Takes a Hit

The Nasdaq suffered a significant decline, driven by rate-sensitive megacap stocks. Companies that have led this year’s rally, such as Nvidia and Microsoft, experienced notable losses, with Nvidia falling 7.3% and Microsoft dropping 1.2%. The Philadelphia SE Semiconductor index also dropped by 5.7%, dragging the broader tech sector down by 3.3%. This decline highlights the vulnerability of tech stocks to economic data and interest rate speculation.

Labor Market Reports in the Spotlight

Traders are now focusing on upcoming labor market reports, with Friday’s non-farm payrolls data for August being a critical focus. July’s employment report had already hinted at a potential slowdown, which led to a global stock selloff earlier in the month. Investors are particularly interested in these labor reports as they could shape the Federal Reserve’s approach to monetary policy. The odds of a 25-basis point interest rate cut stand at 63%, with a 37% chance of a more substantial 50-basis point cut, according to the CME Group’s FedWatch Tool.

Market Sentiment and Defensive Stocks

Amid the market’s downturn, some defensive sectors saw marginal gains. Consumer staples, healthcare, and utilities increased, offering a haven for cautious investors. Wall Street’s fear gauge, the CBOE Volatility Index, rose to an over one-week high, indicating growing market anxiety. Despite the decline, some bright spots, such as Tesla, saw a slight increase after news of a new six-seat variant of its Model Y car set to be produced in China.

Uncertain Path Ahead

The start of September has brought renewed uncertainty to Wall Street, with economic data playing a crucial role in shaping market sentiment. As Josh Jamner pointed out, while the latest data is not what many had hoped for, Friday’s employment figures will be a crucial indicator of the direction the Federal Reserve might take. With a mix of gains and losses across different sectors, investors remain watchful, assessing each new piece of information to navigate these uncertain times.